1. Introduction

Food price volatility endangers farmers and consumers globally. Rapid food price changes impede traders’ ability to determine appropriate stock levels and set appropriate prices. Among other things, food price volatility is equivalent to a nonfunctioning food system. Therefore, excessive price volatility is undesirable, given that food price variability is a feature of most food systems; such variability reflects producer and market responsiveness to consumer demand and underlying supply conditions. However, some exogenous factors have been identified as potential sources of food price variability, namely the presence of weak institutions (Bora et al., 2011), political instability (Minot, 2014), climate change (Kalkuhl et al., 2016), market failures (Timmer, 2017), and some emerging diseases such as COVID-19 (Devereux et al., 2020). It is worth noting that the extent to which these factors impact food price volatility cannot be generalized. For instance, although Africa contributes the least to global emissions of greenhouse gases (GHGs), the food price effects of climate change are expected to be relatively more challenging in Africa, whose rain-fed agriculture is susceptible to climate variability (see Woetzel et al., 2020). Since the interaction of temperature and precipitation is a crucial factor of grain crops’ productivity, the relatively more frequent extreme rainfall in Africa, coupled with other features of climate change, could increase the variability of grain production and the volatility of food prices in Africa. However, it is unclear whether to limit the exogenously induced food price volatility to climate change in an economy whose agriculture is vulnerable to both climate change and domestic unrest (terrorism and banditry).

Nigeria is ranked among the top ten African economies with the highest incidence of climate change and is globally ranked by the Global Terrorism Index (GTI, 2022) as the 8th economy with the highest impact and incidence of terrorism. A growing assertion has linked Nigeria’s recent food price fluctuations to the insurgence of armed banditry, terrorism, militancy, and kidnapping. The underlying intuition is that the unprecedented rise in insecurity associated with these social vices has displaced farming communities and hindered cultivation, leading to higher food prices and increased reliance on imports. Concerned by this undesirable vulnerability of Nigerian agriculture to domestic unrest, we hypothesized that terrorism—and not climate change—is the exogenous underlying source of excessive food price volatility in Nigeria. Fasanya & Odudu (2020) model volatility spillover among different food prices, and Gardebroek & Hernandez (2013) model volatility spillover between food prices and other commodity prices. Understanding the extent of Nigeria’s food price volatility, which is exogenously induced by climate change and terrorism will provide policymakers with evidence-based insight to promote designing and implementing measures to mitigate the vulnerability of agricultural activity to these exogenous factors. This is the contribution of this study and we aim to distinguish between realized and exogenously induced food price volatility. We employ a Generalized Autoregressive Conditional Heteroscedasticity framework with Mixed Data Sampling (GARCH-MIDAS) to distinguish between realized and exogenously induced food price volatility. More importantly, the GARCH-MIDAS model enables data accommodation in their natural frequency and overcomes the likelihood of information loss associated with data aggregation into a uniform frequency (i.e., data splicing).

The rest of the paper is structured as follows: Section II discusses the data and offers some preliminary analyses; Section III presents the methodology; Section IV presents the results and discusses the findings. Finally, Section V contains the conclusions.

II. Data and Preliminary Results

Monthly food prices, our high-frequency variable, range from January 1995 to December 2022, while annual climate change is measured in terms of temperature anomalies, and the annual Terrorism Index defines our low-frequency variable. To capture the probable volatility dynamics of food prices, we follow the standard practice in the literature; the natural logarithm of the first difference of food consumer price index (FCPI) is obtained from the online database of the Nigerian National Bureau of Statistics (NBS). The climate change data is obtained from the Food and Agriculture Organization’s (FAO) online database. The terrorism data based on the GTI database is obtained from the Institute for Economics and Peace. We evaluate the statistical features of these variables of interest to validate the appropriateness of our chosen estimation technique to model food price volatility. Starting with the summary statistics, a cursory look at Table 1 shows that the average monthly food price index is 147.7 for the period under consideration. However, the fact that the mean value is positive for the FCPI also holds for the climate change and terrorism variables, respectively.

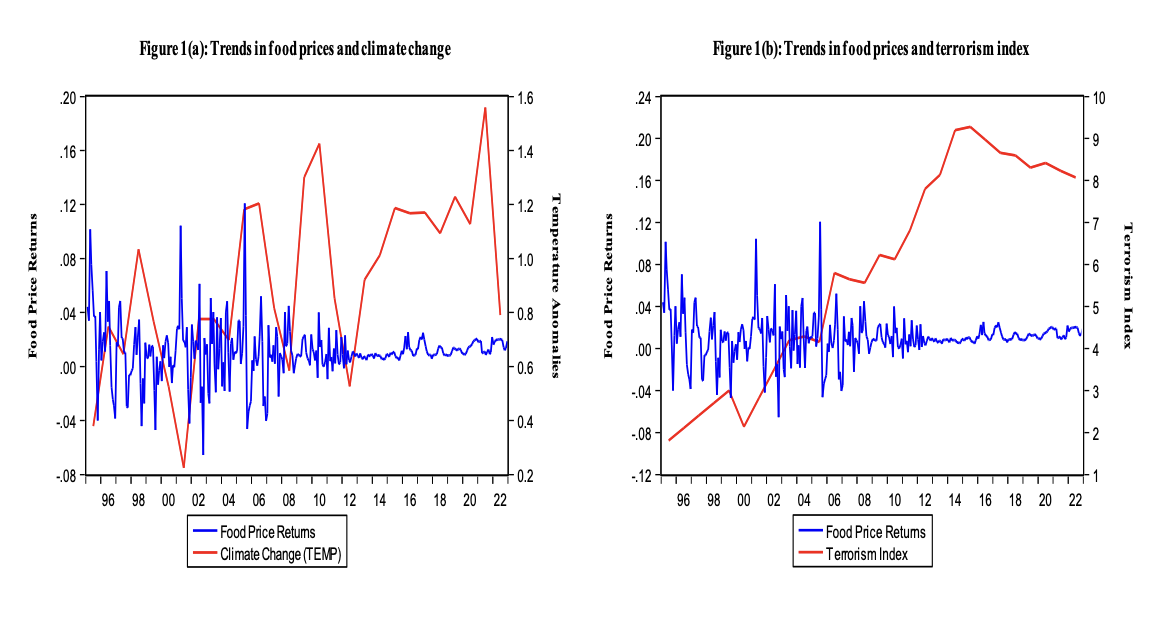

The standard deviation statistic value Is relatively higher for food prices and terrorism activity, suggesting that both are more volatile than the climate change variable. However, while the skewness statistic is positive for food prices, it is negatively skewed regarding climate change and terrorism variables. Similarly, the kurtosis statistic is leptokurtic for food prices but platykurtic for climate change and terrorism variables. Testing for conditional heteroscedasticity and autocorrelation, we find a null hypothesis of homoscedasticity and no autocorrelation rejected for food prices at different lag lengths. However, the fact that these results do not hold for climate change and terrorism may be connected to the mixed-frequency nature of our variables given that statistical features such as heteroscedasticity and autocorrelation are standard with high-frequency series—in this case, food prices. Despite the mixed findings in the preliminary result, our dependent and high-frequency variable, food prices, is characterized by volatility. Thus, the choice of our estimation technique is appropriate as demonstrated below. We complement our preliminary analysis with a visual illustration of probable co-movement between food prices, climate change, and terrorism (see Figure 1).

III. Methodology

Given the monthly and annual mixed frequencies of our variables of interest, we prefer the MIDAS variant of the GARCH models (i.e., GARCH-MIDAS). While the GARCH component of the GARCH-MIDAS accommodates the volatility dynamic of the data, the MIDAS component allows us to retain the natural frequency features of our variables of interest. The following is our GARCH-MIDAS econometric framework.

ri,t=μ+√τt×hi,tεi,t,εi,t∣Φi−1,t:N(0,1),∀i=1,…,Nt

hi,t=(1−α−β)+(ri−1,t−μ)2τi+βhi−1,t

τ(rω)i=m(rω)+θ(rω)K∑k=1ϕk(ω1,ω1,)X(rω)i−k

Equation (1) is our mean equation, and Equations (2) and (3) capture the conditional variance of our GARCH-MIDAS model for short- and long-run components, respectively. Note that the term in Equation (1) denotes the unconditional mean of food prices. Equation (2) is the short-run component of the conditional variance of our high-frequency variable (i.e., monthly food prices), which aligns with a GARCH process. The terms and denoting ARCH and GARCH effects are conditioned to be positive or at least zero and and sum up to less than a unit The term is the long-run component of the conditional variance that incorporates the exogenous series (or realized volatility, where there is no exogenous series); it involves repeating the annual value through the months in that year. The implementation of a rolling-window framework, which enables the secular long-run component to vary monthly, is denoted by the subscript in Equation (3). Simultaneously, represents the long-run component intercept. Of particular interest in Equation (3) is the slope coefficient which incorporates the predicting power of climate change and terrorism and captures a single exogenous predictor food prices, while is the weighting scheme that must sum up to one for the parameters of the model to be identified.

IV. Empirical Results

The main goal of this study is to distinguish between food price volatility caused by the food system and exogenously induced food price volatility. The GARCH-MIDAS-based empirical estimates presented in Table 2 show that the coefficient on the parameter which captures the unconditional mean of food price, is positive irrespective of the variant of the GARCH-MIDAS models. We also found the volatility persistence coefficient measure – the sum of the ARCH and GARCH terms, for instance – to be as high as 0.90 in each variant of the GARCH-MIDAS models. This indicates that short-term food prices exhibit the highest level of persistent volatility, confirming our preliminary finding regarding the inherent fluctuations in food prices. Concerning the focal point of this study, the slope coefficient - is statistically significant for the realized volatility (RV) in the GARCH-MIDAS-RV model. The RV has a positive effect on long-term food price volatility, which suggests that the bigger the fluctuation in the RV, the bigger the long-term volatility in food prices. However, the slope coefficient on the exogenous factor is only statistically significant when the in the GARCH-MIDAS-X represents terrorism. These validate our hypothesis that terrorism, and not climate change, exogenously induces food price volatility in Nigeria. More importantly, our findings support Fasanya and Odudu’s (2020) study, which recognizes the crisis period as the underlying source of volatility in agricultural commodity prices in Nigeria. We showed that the exogenous factors, particularly the terrorism index, offers insights beyond the realized volatility of food prices.

V. Conclusions

We employed a GARCH-MIDAS framework to distinguish between realized and exogenously induced food price volatility. Compared to climate change, we confirm that terrorism is the fundamental factor that exogenously induces food price volatility in Nigeria. Although policymakers should not restrict their initiative to curb excessive food price volatility to modify food demand and supply, they should also consider some exogenous factors capable of inducing food price volatility. It is important to note that the impact of climate change and terrorism on various components of the food basket may not be uniform. Therefore, future studies should consider conducting separate analyses for major food items that significantly impact overall food price volatility.